The 2024 Budget Forecast Return (BFR) brings significant changes that require Multi-Academy Trusts (MATs) to split ICT expenditure across several new categories. This blog provides expert guidance on managing these changes, including detailed steps for handling the current year’s forecast, strategies for future budgeting, and the benefits of using IMP Software’s BFR wizard. By understanding and implementing these new requirements, trusts can ensure accurate and efficient financial reporting, aligning their budgets with the latest Department for Education (DfE) guidelines.

Changes in this year’s BFR Structure

As most trusts are finalising their 2024/25 budgets and preparing for the BFR submission to the DfE, it’s crucial to understand the significant changes in this year’s BFR structure. In recent years, the BFR structure has remained relatively static; however, the 2024 BFR introduces substantial changes that require some thought concerning managing these changes in your budgeting system.

We have seen the introduction of seven new revenue ICT categories and five new capital ICT categories, with reporting of these new budget splits required from the current forecast year 2023/24 onwards.

Although these categories have been available since the end of April, the updated DfE Chart of Accounts (COA) with new account codes mapping directly to these categories was only released on 18th June. This late availability poses a challenge for trusts to analyse budgets across multiple new categories in a short timeframe.

For more information on all the changes in the BFR, refer to the DfE BFR Guidance.

Current Year 2023/24 Forecast

Most trusts use their March forecast for the BFR submission. However, with the ICT split changes announced post-March, trusts find their actuals and remaining forecast data not categorised as per the new reporting requirements. The new COA codes are not a direct one-to-one mapping from old to new codes, leading to costs in existing account codes relating to multiple BFR classifications.

To manage this you will need to extract and analyse the data driving your March forecast on a line-by-line basis for each transaction in your seven-month actuals and each forecast line for the remaining five months. Use these new categorisations to populate the 2023/24 element of the BFR.

You should ensure you address this promptly ahead of the 29th August submission deadline.

2024/25 Onwards

For 2024/25 and all future years, budgets will need to be split to reflect where ICT expenditure should now be apportioned.

Splitting and reallocating specific budget lines to new account codes is essential. While most trusts are nearing the end of the budget-setting cycle, this task could have been simpler if the new COA had been released earlier!

Benefits of Early Action

- Direct mapping of budgets against the new account codes for the BFR.

- Your budgets will be sat in the right place ahead of next year and thus when you get to the point where you are recording actuals and subsequently producing your management accounts and forecasts, budgets and actuals will be aligned and treated consistently.

If your budgets are already approved and subsequently frozen/locked so changes cannot be made, you may need to split your budgets manually in the BFR. This manual adjustment might cause issues in the next fiscal year, so finding a way to reflect these changes in your approved budget scenario is crucial. Ensure all changes are reflected in both your accounting system and your budgeting tool.

Trustees approved the changes, and revisions to financial regulations were made to support the new funding model.

Don’t Forget

With the end-of-August submission date now seemingly permanent, consider your submission timing around pay award announcements i.e. before or after pay award announcements. Last year, we provided guidance on various options, which remains relevant: Access last year’s guidance here.

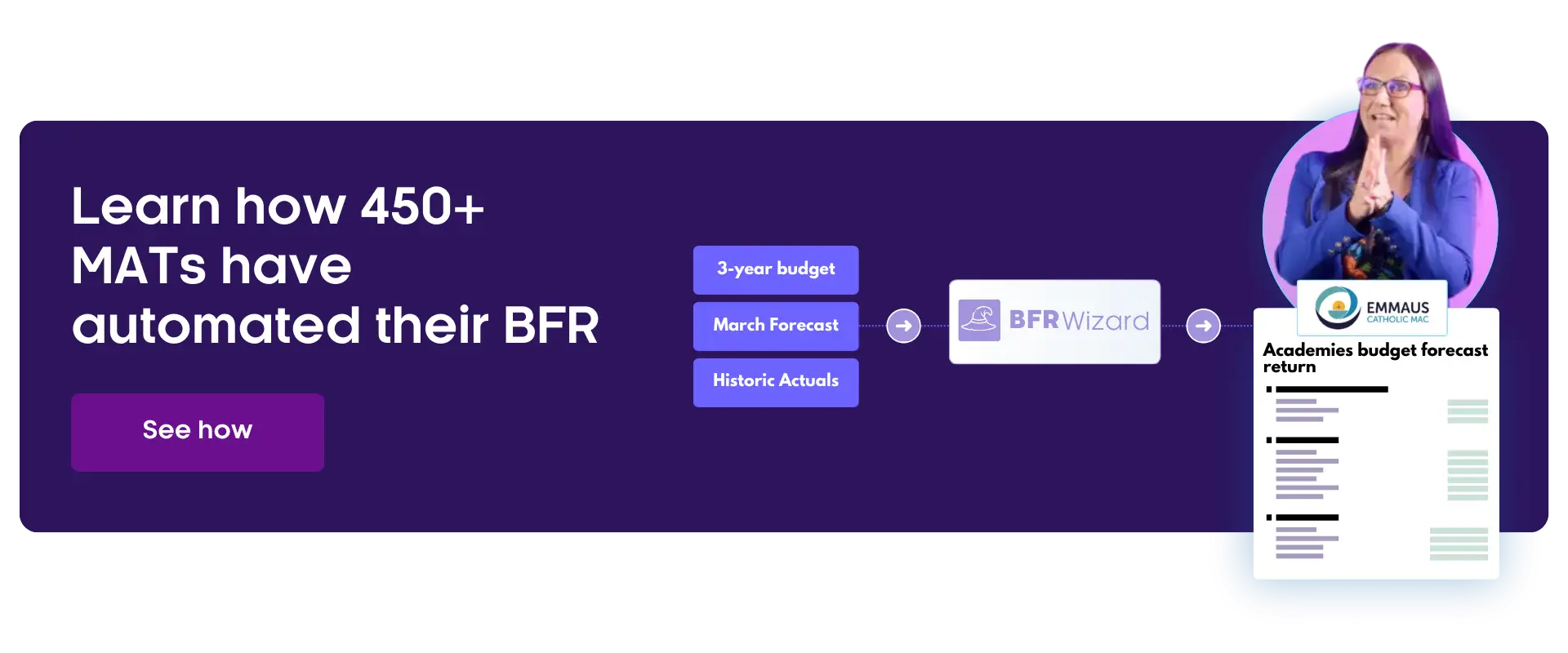

IMP BFR Wizard and Support

We understand that the BFR submission can be unwieldy and with the added complication and timing of these changes, the headaches this year are likely to be exasperated. At IMP, we stay ahead of all BFR updates, and our BFR wizard is optimised to help customers navigate these new requirements, ensuring that the production of the BFR is as seamless as ever.

Our BFR wizard is an innovative tool that we have developed over the past few years to automate the collation, mapping and population of the BFR form. IMP Planner is the only tool that is natively designed to combine the historic actuals from the finance system, with the March forecast and the forward-looking 3-year budget, eliminating manual data entry and consolidation, it significantly reduces the time and effort required to prepare the BFR submission.